![]()

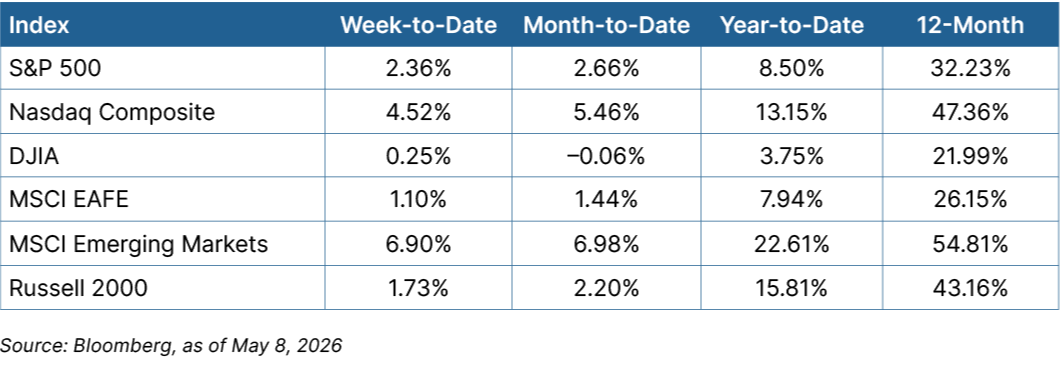

The Nasdaq led markets higher; the Russell 2000 rose for the sixth consecutive week.

Institute for Supply Management (ISM) Services Index:

April (Tuesday)

Service sector confidence fell slightly last month. New order growth slowed, but business activity increased.

- Expected/prior month ISM Services index: 53.7/54.0

- Actual ISM Services index: 53.6

Employment Report:

April (Friday)

Last month’s employment report showed continued healthy job growth, with 115,000 jobs added against expectations for 65,000.

- Expected/prior change in nonfarm payrolls: +65,000/+185,000

- Actual change in nonfarm payrolls: +115,000

Preliminary University of Michigan Consumer Sentiment Survey:

May (Friday)

Consumer confidence fell more than expected, marking the second consecutive month in which the index has set a new low, signaling potential headwinds for consumers.

- Expected/prior month sentiment: 49.5/49.8

- Actual consumer confidence: 48.2

Equity

U.S. equity markets were again led higher by the Nasdaq Composite, which rose more than 4 percent, and the S&P 500, which was up more than 2 percent. Both indices closed at record highs. Markets were paced by the technology sector, which rose 7 percent. With news about the potential for a negotiated end to the Middle East conflict, energy declined more than 5 percent and materials fell roughly 4 percent. International markets finished higher, rising about 1 percent.

Fixed Income

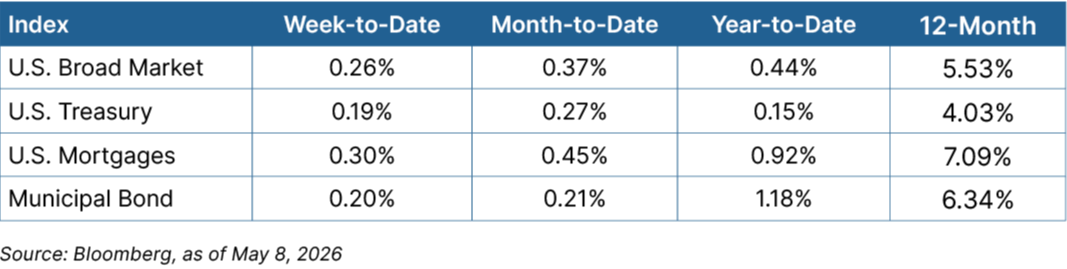

Fixed income markets were mostly higher, with the broad market up marginally. Markets reacted favorably to a stronger-than-expected jobs report, which should give the Fed time to remain data-dependent before changing interest rates. The 10-year Treasury yield was essentially flat, closing at 4.35 percent. Municipal bond yields were down slightly.

Looking Ahead

Inflation data returns to the spotlight this week. Consumer and producer prices are expected to show increases as elevated oil prices continue to drive inflation higher.

- The week kicks off Tuesday with the Consumer Price Index for April. Elevated oil prices are expected to lead to another increase in prices paid by consumers.

- On Wednesday, we’ll see the Producer Price Index for April. As higher oil prices begin to work their way through supply chains, it’s expected that the prices producers are paying will increase, perhaps to 5 percent.

- On Thursday, we’ll have a look at retail sales for April. It’s anticipated that sales will be strong for the fourth month in a row, which would be a positive sign for the consumer-driven economy.

- A strong first-quarter earnings season is wrapping up, with reports expected from Simon Property Group, ON Semiconductor, Cisco, and Applied Materials.